10 Mins

Modern borrowers look for speed and convenience in their lending experience. Field verification slows it down.

On an average it takes 3-5 days for an agent to complete the field verification process. It not just slows down the onboarding process, it hands your borrower over to whoever verifies them first. They don't call to complain. They don't ask for an update. They simply move on. It's a quiet revenue leak that never shows up on a dashboard.

Field verification was convenient for low volumes, but it fails to scale with the increasing volume of applications.

The rest of the lending stack has already been modernised. Bureau checks can be run in seconds. Video KYC happens in minutes. E-sign has made physical paperwork obsolete. Field verification is the last step running on a model from a decade ago, and it's the one sitting between you and your approved borrowers.

In this blog, we break down why field verification fails at scale, and how Digital Contact Point Verification closes this gap with a 10-minute, mobile-first flow that keeps borrowers moving forward, not waiting.

Why field verification breaks down at scale

The model wasn't designed for current lending volumes or borrower expectations. Here's where it consistently fails:

Geographic gaps. Tier 2 and Tier 3 applicants, the core growth segment for most NBFCs , often sit outside cost-effective field coverage. The average cost for field verification is approximately ₹300 – ₹700 per address. Sending an agent to a semi-urban address is not a cost effective step especially for low-ticket loans.

Scheduling friction. A field visit requires two people in the right place at the right time. One missed attempt becomes three. A one-step verification turns into a multi-day back-and-forth that sits entirely outside the control.

Inconsistent documentation. Field agents capture photos and transcribe data manually. Quality varies across agents and geographies, blurry document scans, address mismatches, incomplete forms. These inconsistencies don't just slow processing; they create compliance exposure.

Audit risk. A folder of JPEGs and handwritten field notes is not held reliable under regulatory scrutiny. Structured, timestamped, traceable documentation is increasingly the expectation, and physical field ops rarely produces it by default.

The impact of failed field verification

The obvious cost is speed. A 3-7 day field cycle creates a window where you are not the only lender the borrower is talking to.

But the compounding costs are more damaging:

Per-verification cost. Agent time, travel, coordination overhead, and repeat visits add up significantly at scale. For NBFCs processing high volumes across non-metro geographies, this is a material ops line item, one that doesn't shrink as the portfolio grows.

Structural exclusion from Tier 2/3. If your field network can't cover these geographies cost-effectively, you're not just losing individual applications. You're locked out of a growth segment at the portfolio level.

Compliance overhead. Inconsistent field documentation creates downstream work for compliance and legal teams, and real risk if it surfaces in an audit.

Digital Contact Point Verification: Remote, structured, and borrower-led verification

The question isn't "how do we make field verification faster?" It's more fundamental: why does contact point verification require a physical agent at all?

The purpose of the field visit is to confirm specific things, the borrower is a real person, they are who they claim to be, they are located where they say they are, and their documents are genuine. These are data problems. Data problems can be solved digitally.

The borrower receives a link on their phone. They complete a structured verification flow, from wherever they are, at a time that suits them, in under 10 minutes. The flow captures the same underlying data as a physical visit: location, identity, document authenticity. Every data point is timestamped, geotagged, and stored in a structured format. The output isn't a folder of photos, it's a clean, auditable verification record that slots directly into your LOS.

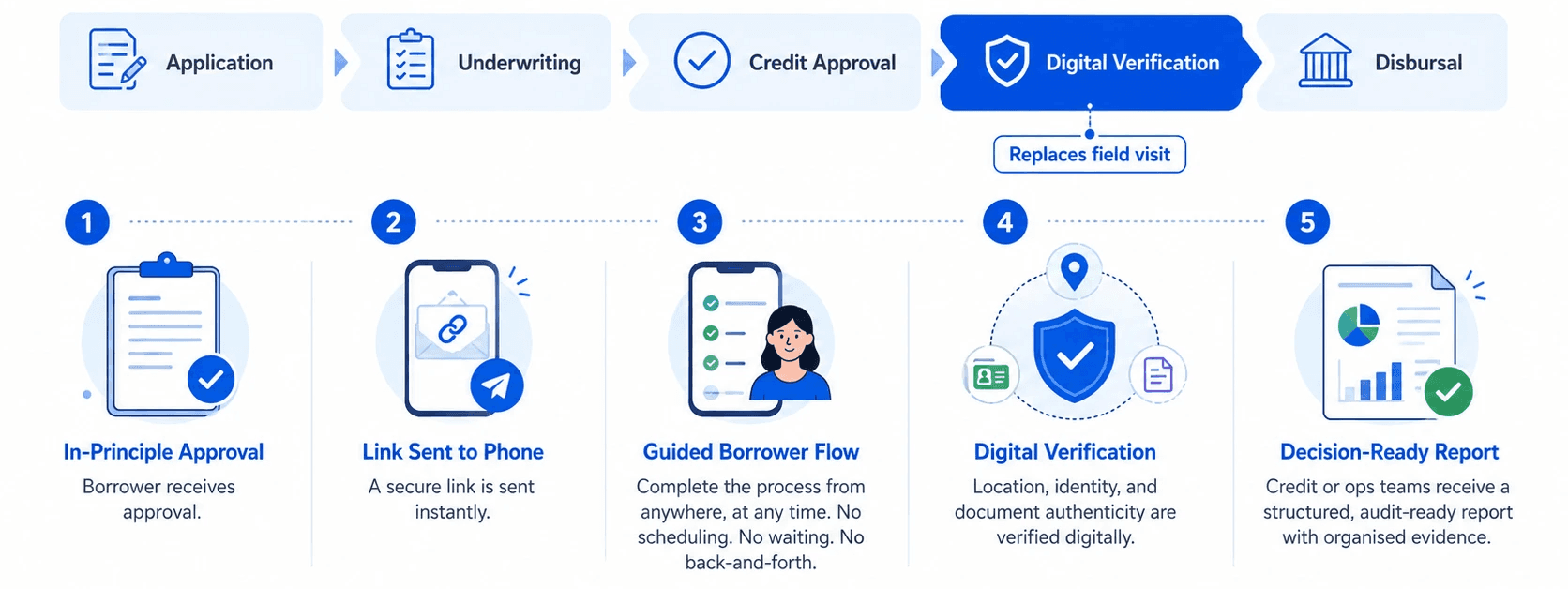

How it works and where it fits in your onboarding flow?

This is designed to replace the field visit at the exact point in your onboarding where it currently sits: post-credit approval, pre-disbursal.

Here's what the digital contact point verification looks like in the onboarding flow:

Here's what happens:

Send a link. That's the whole initiation. Your team creates a verification session and sends the borrower a link via SMS or email. No agent assignment, no scheduling calls, no back-and-forth. The borrower picks it up when it suits them — or schedules it within 2 days if needed. Hourly reminders handle the follow-up automatically.

The borrower does the fieldwork — from their phone. Live location. House photos. Utility bill or rent agreement. ID proof. Optional face verification. It's a guided, sequential flow that captures everything a field agent would — in under 10 minutes, from wherever the borrower is.

Your system does the verification — instantly. OCR, geo-consistency checks, document validation, fraud indicators, cross-signal triangulation. All automated, all running in the background before your ops team even looks at the case.

What lands in your queue is a decision, not raw data. A structured report with a clear status; Verified, Failed, Needs Review, or Cannot Complete, along with risk flags, reason codes, timestamped evidence, and a PDF audit trail ready for underwriting or compliance.

The entire borrower-side experience takes under 10 minutes. For your ops team, it replaces a 3-7 day coordination cycle with a same-session output.

What changes when you deploy this?

Speed. The same day a borrower receives in-principle approval, they can complete contact point verification from their phone. The 3-7 day field cycle can be implemented as a 10-minute same-session step within the access of the borrower.

Cost. Agent travel, coordination, and repeat visits are eliminated for every application routed through the digital flow. The cost reduction per verification is significant at any meaningful volume.

Coverage. Geographic constraints disappear. A borrower in a semi-urban district completes the same verification flow, with the same quality output, as a borrower in a metro. Your field network's reach is no longer the ceiling on your serviceable market.

Compliance. Every verification produces the same structured output, timestamped and complete, without additional work from your ops or compliance teams.

See it in your onboarding stack

Field verification is your longest onboarding leg, it doesn't have to be. Digital Point Contact Verification by Tartan integrates seamlessly into your existing onboarding flow at exactly the point where the field visit currently sits, without rebuilding your process.

To see the solution in action - Book a Demo

Tartan helps teams integrate, enrich, and validate critical customer data across workflows, not as a one-off step but as an infrastructure layer.