10 Mins

In 2024, IRDAI replaced 37 existing regulations with 7 consolidated ones. New product regulations came into force on April 1, 2024. The Insurance Products Regulations 2024 mandated Board-approved product management governance, new pricing principles, and mandatory Product Management Committees - all effective immediately.

The Insurance Laws Amendment Bill, tabled at the end of 2024, proposes changes significant enough that industry publications called it a potential reshaping of the entire regulatory framework.

That is not a slow year of regulatory change. That is a structural overhaul arriving faster than most insurers' internal change processes are designed to absorb.

And yet the question that rarely gets asked in the boardroom conversation about regulatory compliance is this: between the date a regulatory change is notified and the date that change is live across every channel your product is sold and serviced through - web, branch, aggregator, API, agent - how many days actually pass?

For most Indian insurers, the honest answer is uncomfortable.

The journey from circular to live

When IRDAI issues a regulation or circular, the clock starts. The insurer's legal and compliance team reads it, interprets it, and produces an internal note on what needs to change.

That note goes to the product team. The product team assesses the impact - which products are affected, which clauses need updating, which pricing parameters need revision, which exclusions need to be reworded.

Then it enters the system. The updated product terms need to be translated into rule engine logic. That goes to the tech team. The tech team is already mid-sprint on three other things. The policy change joins the queue. It gets scoped, developed, tested in staging, and deployed.

Meanwhile, someone needs to update the product prospectus, the sales scripts, the aggregator feeds, and the branch training material.

By the time the change is live everywhere - not just in the policy document, but in the actual decisioning logic, the customer-facing product terms, the claims processing rules, and the distribution channel materials - weeks have passed. Sometimes months.

During that entire window, your product is technically operating under rules that the regulator has already superseded. That is not a hypothetical compliance risk. It is a live one, recurring with every regulatory update, and it scales directly with the pace at which IRDAI issues changes.

"The compliance risk in insurance is rarely about intent. It is almost always about velocity - the gap between when the regulator moves and when the insurer catches up. In 2024, that gap became a liability."

Three specific places this gap creates real exposure

It helps to be concrete about where the deployment lag actually bites, because the risk is not evenly distributed across an insurer's operations.

Claims adjudication. When a regulatory change modifies exclusion criteria, moratorium periods, or claim settlement timelines - as IRDAI's 2024 health insurance guidelines did - claims processed between the notification date and the rule engine update date are being adjudicated under the old logic.

If a claim is rejected based on an exclusion that the new regulation has removed, that is an incorrect decision made by the system.

The insurer is liable for it.

The customer will escalate it.

And the audit trail will show that the insurer was aware of the regulation and had not yet updated their systems.

Product distribution. Aggregators, brokers, and bancassurance partners pull product terms and coverage details from the insurer's systems via API or data feeds. If those feeds have not been updated to reflect a regulatory change, the product is being sold to customers with incorrect terms. The customer's understanding of what they are covered for does not match what the regulation now requires the insurer to provide. This creates mis-selling exposure that is both regulatory and reputational.

Underwriting rules. New pricing principles under the IRDAI (Insurance Products) Regulations 2024 require that pricing reflect risk factors fairly and provide value for money - with actuarial backing for any sub-limits or restrictions. If an insurer's underwriting rule engine has not been updated to reflect these principles, they may be issuing policies at price points or with restrictions that do not comply with the current framework.

Every policy issued during the lag period is potential exposure.

Why this is structurally harder than it should be

The reason policy change velocity is a persistent problem at Indian insurers is not that their teams are slow or careless. It is that the architecture connecting policy documents to live product behaviour is fragmented by design.

Policy and product terms live in Word documents and PDFs - authored by legal and product teams, stored in shared drives or document management systems. The rules that govern how those terms are actually applied - in underwriting, claims, pricing - live in rule engines, configured by tech teams in formats that bear no natural resemblance to the original policy language.

The two are connected only by a manual translation process that requires a human to read the policy document and correctly implement its logic in the rule engine.

Every step in that chain introduces delay and the possibility of error. The legal team interprets the regulation. The product team translates the interpretation into a product change brief. The tech team translates the brief into rule logic. Each translation is a handoff. Each handoff is a point where time passes and accuracy degrades.

Add to this the reality that most insurer tech teams are not sitting idle waiting for policy changes to implement. They are building product features, fixing production issues, and managing ongoing maintenance. A regulatory-driven policy change competes for bandwidth against everything else on the roadmap - and unlike a customer-facing feature, it has no internal champion lobbying for it to be prioritised. It gets done when it gets done.

The IRDAI trajectory makes this problem larger, not smaller

What makes this particularly urgent in 2025 is that the pace of regulatory change is not slowing down. IRDAI's shift to a principle-based framework - replacing prescriptive rules with broader governance principles - gives insurers more flexibility, but it also demands more internal capability to interpret and implement. Where a rule-based regime told you exactly what to do, a principle-based one requires you to demonstrate that your governance framework is sound and your product management decisions are defensible.

The mandatory Product Management Committees introduced under the 2024 regulations are a direct expression of this expectation. IRDAI is asking insurers to build internal governance structures that can translate regulatory principles into product decisions - continuously, not just at annual product reviews.

The insurer that can do this well has a competitive advantage: faster product updates, cleaner compliance posture, and the ability to respond to market changes without waiting for a multi-week change management cycle.

The insurer that cannot do it well has the opposite - a growing gap between regulatory intent and operational reality, with every new circular adding to the backlog.

What fast policy deployment actually requires

Solving this problem properly requires addressing the architecture that causes the delay - not just adding more people to the translation chain.

The core requirement is shortening the distance between a policy document and a live rule. When a regulatory change lands, the question should not be "how long will it take the tech team to implement this?" It should be "can this policy language be converted into executable rule logic directly, with the translation step automated rather than manual?"

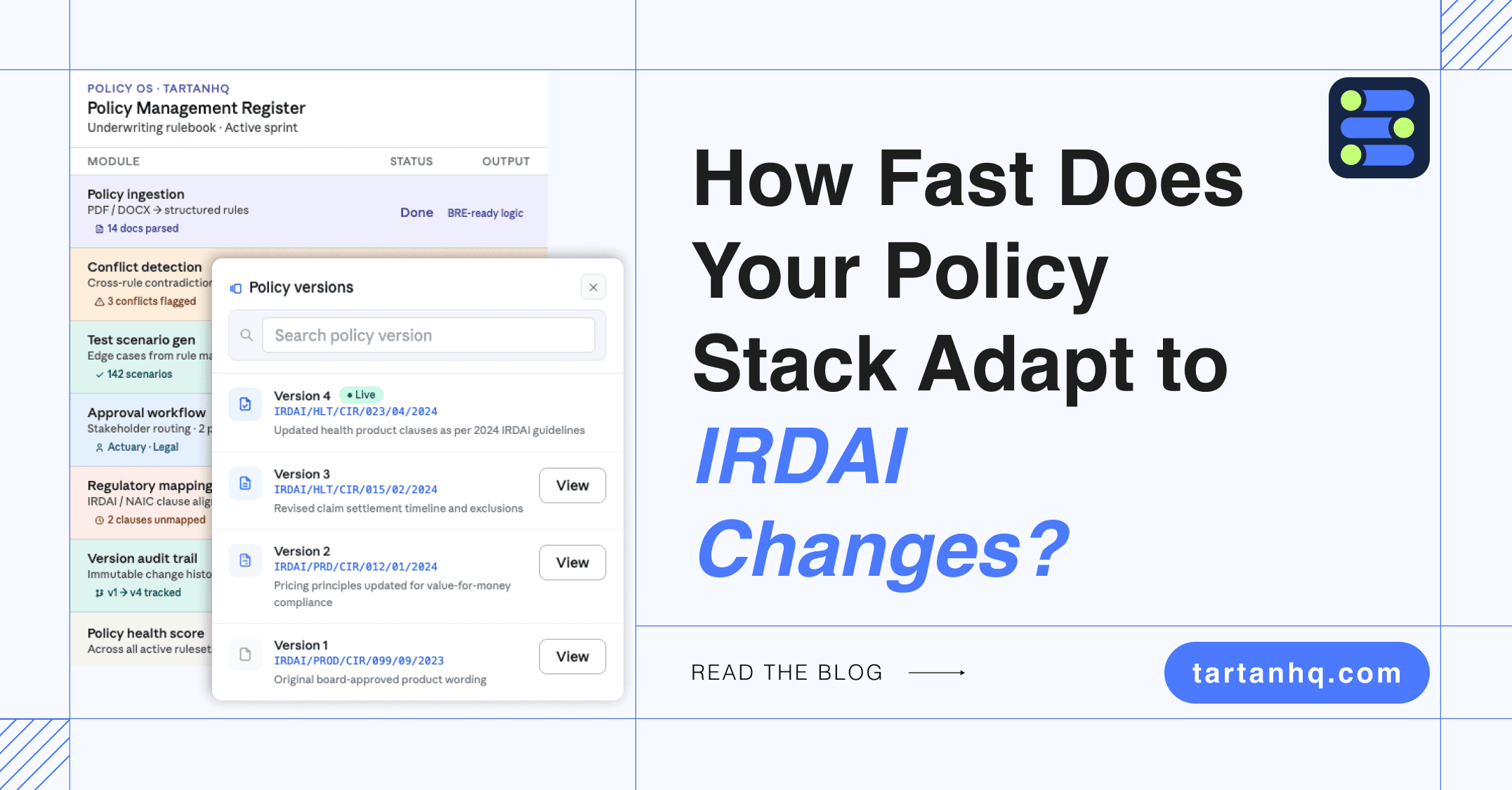

That means having a system that can ingest a policy or regulatory document, identify the rule logic embedded in it, convert it into a format the rule engine can act on, flag conflicts with existing rules, generate test scenarios against edge cases, and deploy - with a full audit trail showing who approved what and when.

The version control dimension matters equally. When a regulator or auditor asks what your exclusion criteria were on a specific date for a specific product, the answer should be retrievable in seconds from a structured log - not reconstructed from a combination of email threads, old policy PDFs, and Jira tickets.

Where PolicyOS fits

This is the specific problem PolicyOS by TartanHQ is built to solve. PolicyOS sits between the policy document and the production rule engine - automating the conversion of policy language into BRE-ready logic, detecting conflicts with existing rules before deployment, running AI-generated test scenarios to validate correctness, and maintaining a version-controlled audit trail of every change.

For insurers managing a product portfolio across multiple lines and distribution channels, PolicyOS compresses the deployment cycle from weeks to days.

The tech team is no longer the bottleneck in the policy change process - the policy change becomes a structured, auditable workflow that the product and compliance teams can drive directly, with engineering effort reduced to oversight rather than transcription.

IRDAI's regulatory velocity is not going to slow down. The insurers building the internal infrastructure to match it - fast policy interpretation, automated rule conversion, clean audit trails - will navigate the next wave of changes with confidence. The ones still relying on the manual chain from PDF to sprint ticket are already running behind.

The question is not whether your compliance team read the circular. It is whether your rule engine has caught up yet.

Tartan helps teams integrate, enrich, and validate critical customer data across workflows, not as a one-off step but as an infrastructure layer.