How repeat borrowers, top-ups, and collections are where identity and address drift actually hurts.

There's a quiet assumption baked into how most digital lenders think about fraud: that it's a gate problem. That the real risk lives at the front door - at the moment a new applicant submits their Aadhaar, links their bank account, and takes their first loan. Lock that door tight enough, and you're safe.

That assumption is costing lenders crores they don't even know they're losing.

The inconvenient truth is that the fraud landscape in digital lending has fundamentally shifted. The most sophisticated, highest-value fraud in the ecosystem today doesn't happen at onboarding. It happens later - quietly, gradually, across the lifecycle of a borrower who already passed your checks. It happens when someone takes a top-up. When they request a limit enhancement. When your collections team tries to reach someone who, it turns out, no longer lives at the address on file - and perhaps never intended to.

This is the problem of identity and address drift. And almost nobody in the industry is talking about it seriously.

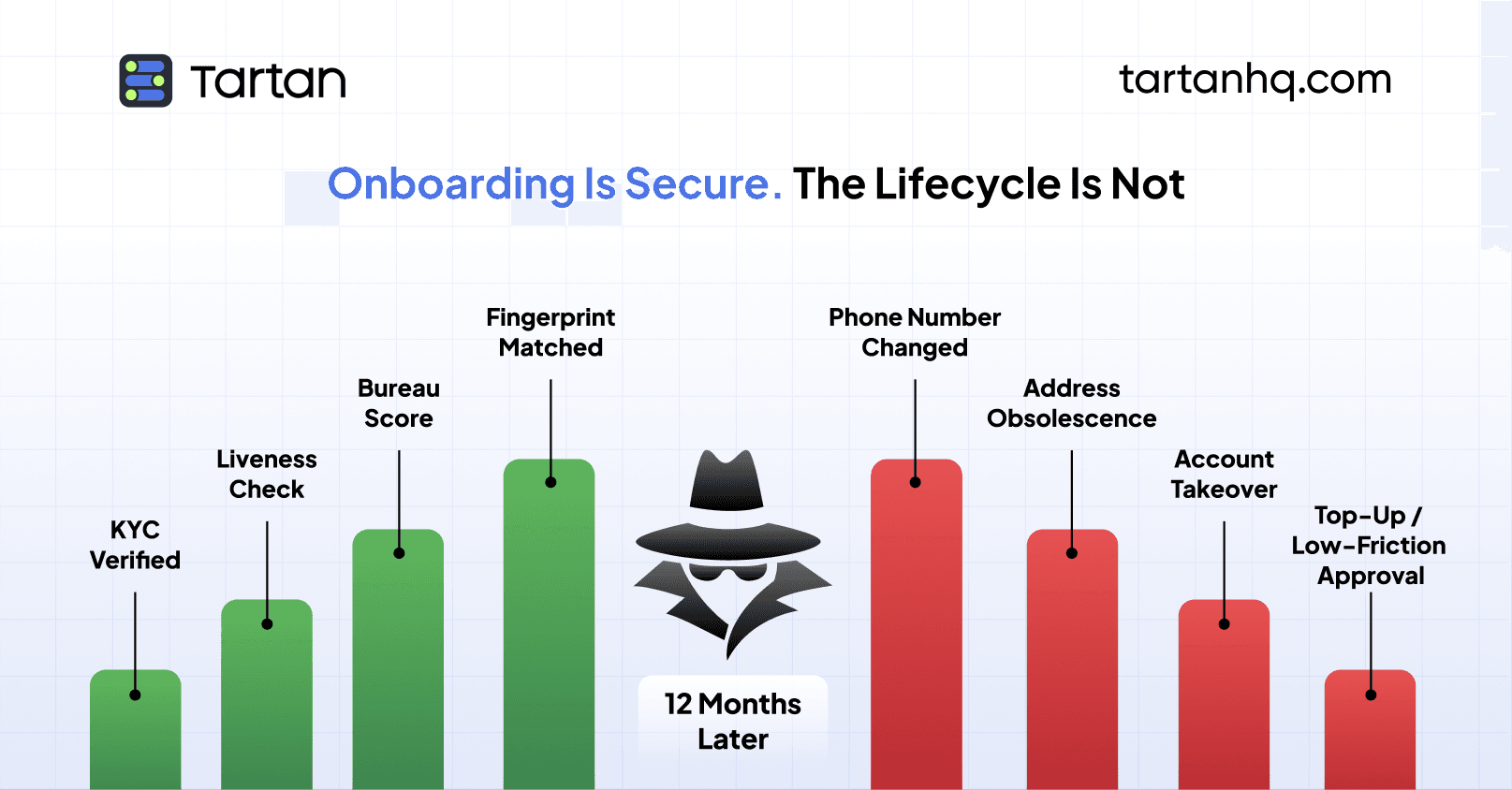

The Onboarding Illusion

The last decade of fintech infrastructure investment has been disproportionately poured into onboarding. KYC APIs, video verification, liveness detection, bureau pulls, device fingerprinting - the average digital lender today runs a new applicant through more checkpoints than a mid-sized bank ran five years ago.

That investment made sense. Early digital lending fraud was brazen: synthetic identities, stolen documents, mule accounts. Plugging those gaps at the front was urgent and necessary.

But here's what happened as a result: fraud adapted. Fraudsters aren't fighting strong onboarding stacks anymore. They're going around them.

The easiest way to beat a rigorous onboarding check is to pass it legitimately - or to wait. Take a small first loan. Repay it. Build a clean repayment history. Earn trust. Then, twelve months later, when you're eligible for a ₹3 lakh top-up with minimal re-verification, make your move. Or sell the account. Or simply vanish.

This is not a theoretical threat. Collections teams at mid-size NBFCs and digital lenders will tell you - off the record - that a meaningful portion of their hard-to-recover accounts are from borrowers who had clean early histories. The fraud didn't announce itself upfront. It was patient.

What "Identity Drift" Actually Means

Identity drift is when the person interacting with your system today is meaningfully different from the person you onboarded - either because their circumstances changed, because the account was taken over, or because the identity was always a vehicle for eventual fraud.

It shows up in several ways:

Phone number churn. Mobile numbers in India get recycled. A borrower's verified mobile number from eighteen months ago may now belong to someone else entirely - and your OTP-based authentication doesn't know the difference. If that number is the primary factor for loan access, you have a gap.

Account takeover via credential compromise. Especially as lending apps scale to tier-2 and tier-3 markets, borrowers reuse passwords, use shared devices, and are susceptible to phishing. A legitimate account taken over by a bad actor is invisible in your onboarding data.

Address obsolescence. People move. That's normal. What isn't normal - but is systematically ignored - is that most lenders never update address data after onboarding. The address on file at the time of a top-up is often the one captured eighteen months ago. When the borrower defaults and collections steps in, the address is wrong. Not because the borrower deliberately lied. Because no one ever asked again.

Deliberate drift by organized fraud rings. More sophisticated operations deliberately let an account "age" with small repayments before updating contact details to redirect communications, gradually shifting control before a large drawdown.

The Top-Up Trap

Top-up loans are, for lenders, a beautiful product. The economics are compelling: you're lending more to someone you already know, with a repayment history, without the full cost of acquisition or onboarding. Approval is faster, documentation lighter, friction lower.

That lower friction is exactly what makes them dangerous.

Most lenders apply significantly less scrutiny to a top-up than to an initial application. The re-KYC, if it happens at all, is cursory - a selfie check, an OTP, a quick bureau pull. Address re-verification? Almost never. Identity freshness checks? Not standard practice.

But consider what's changed between the first loan and the top-up: time. Sometimes a lot of it. The risk profile of a borrower eighteen months into a lending relationship is genuinely different from their profile at origination - and not always in the direction you'd hope.

Bureau scores lag. A borrower could be three months behind on a different lender's obligation, but that might not have surfaced in your data yet. Their employment situation may have changed. Their phone number may have churned. Their address may be stale. And if their account has been quietly taken over, you may be handing ₹2 lakh to someone you've never actually verified.

The top-up, designed to reduce friction, has become a preferred point of attack precisely because lenders have optimized it to have fewer checks.

Collections: Where the Damage Becomes Visible

If top-ups are where drift creates risk, collections are where it creates losses.

By the time a borrower is in default and collections engages, the lender's leverage depends almost entirely on being able to reach the borrower. Phone number. Address. Employer. Emergency contacts. That data, captured at onboarding, is now the operational foundation of your recovery effort.

And it rots.

According to internal estimates shared by collections vendors working across the Indian digital lending space, a meaningful percentage of contact details go stale within 12–18 months of capture. In a lending book where average tenures stretch that long, that's a significant portion of your hard bucket accounts with unreliable contact data.

But the issue runs deeper than operational inconvenience. Stale address data also creates compliance exposure. Regulatory norms around collections conduct require lenders to make genuine, documented attempts to reach borrowers. If your address is wrong and your phone number is dead, your collections effort is both ineffective and potentially non-compliant - you can't demonstrate reasonable outreach.

And when the address was wrong not because the borrower moved, but because the identity was drifted or stolen, you're not just dealing with a bad debt. You're dealing with a fraud case that your collections infrastructure is the first to discover - eighteen months after your onboarding stack said everything was fine.

The Verification Gap Nobody Talks About

Here's what's strange: lenders have invested heavily in point-in-time verification at onboarding, but almost nothing in continuous or periodic re-verification across the loan lifecycle.

This creates a structural gap. Your system knows who the borrower was on day one. It has no reliable mechanism to know who they are on day 400.

Some lenders do trigger re-KYC at top-up, but the bar is low - usually a selfie liveness check and an OTP. That catches the most basic account takeovers, but not phone number churn (because you're sending the OTP to the potentially compromised number), not address drift, and not the kind of gradual identity migration that sophisticated fraud rings execute.

What would actually help is a layer of continuous identity hygiene: periodic checks against authoritative sources to confirm that the mobile number, address, and identity markers on file still match what the underlying databases reflect. Not just at onboarding. Not just at top-up. Across the lifecycle, at key trigger points - limit enhancements, top-up requests, unusual device changes, and pre-collections escalation.

This isn't science fiction. The data infrastructure to support it exists. What's been missing is a product that operationalizes it simply enough that lenders can embed it without rebuilding their tech stack.

The Borrower Journey Deserves Fraud Controls That Match

Fraud doesn't respect the internal org chart that separates your onboarding team from your collections team. It operates across the full borrower lifecycle, and the weakest link is wherever you've stopped checking.

Right now, for most digital lenders, that weakest link is everywhere after onboarding. Top-ups. Limit enhancements. The moment a collections agent picks up a file and realizes the phone is dead and the address is a vacant plot.

The industry needs to retire the mental model of fraud as a gate problem and replace it with fraud as a lifecycle problem. That means verification architecture that follows the borrower through origination, servicing, and recovery - not just through the front door.

How HyperVerify Addresses This

HyperVerify to close exactly this gap.

HyperVerify is a continuous identity and address verification layer designed for the full lending lifecycle - not just onboarding. It enables lenders to run real-time verification checks at any trigger point: before a top-up is approved, before a limit enhancement goes through, or as a pre-collection intelligence step on defaulted accounts.

At its core, HyperVerify does three things that most point-in-time KYC solutions don't:

Live address verification against authoritative databases, so lenders know whether the address on file is still valid before they disburse a top-up or dispatch a field agent.

Mobile number freshness checks, confirming whether the registered number is still associated with the expected identity - catching the phone churn problem that OTP-based re-authentication cannot.

Identity continuity signals that flag anomalies between what's on file and what current data sources reflect - surfacing potential account takeovers or identity drift before they become defaults.

For collections teams, HyperVerify provides enriched contact intelligence on hard-to-reach accounts - current likely address, active number status, and identity confidence scores - giving agents better data before first contact and helping lenders meet their compliance documentation requirements.

The product is API-first, designed to embed into existing loan management systems and collections workflows without heavy integration work.

For lenders who've spent years hardening their onboarding stack, HyperVerify is the piece that closes the back door - the one that's been quietly open the whole time.

Fraud evolves. Your verification strategy should too. The borrower you onboarded eighteen months ago and the account active in your system today may not be the same person. It's time to build like that matters.

Tartan helps teams integrate, enrich, and validate critical customer data across workflows, not as a one-off step but as an infrastructure layer.