In today's hyperconnected financial ecosystem, organizations face an escalating challenge: how to integrate with dozens - sometimes hundreds - of different software systems without drowning in technical complexity. Enter unified APIs, a transformative approach that's reshaping how banks, fintech companies, and insurance providers build and scale their digital infrastructure.

Understanding the Integration Crisis

Picture this scenario: Your fintech platform needs to offer customers the ability to connect their payroll accounts. But your customers use ADP, Gusto, Paychex, BambooHR, Workday, and dozens of other payroll providers. The traditional approach would require your engineering team to:

Build separate integrations for each payroll system

Learn the unique authentication methods, data structures, and API conventions of each provider

Navigate varying documentation quality and API design philosophies

Maintain these integrations as each provider releases updates and breaking changes

Debug issues across multiple different error-handling approaches

Research indicates that organizations typically take at least three weeks to launch a single integration. For a platform targeting enterprise customers who might use any of 40+ different payroll systems, this traditional approach becomes mathematically untenable. The engineering resources required would be staggering, and the maintenance burden would grow exponentially.

This is the integration crisis, and it's particularly acute in banking, fintech, and insurance - industries where data flows between multiple systems are not just common but essential to operations.

What is a Unified API?

A unified API is a single, standardized interface that consolidates multiple APIs from similar software systems into one consistent endpoint. Rather than integrating directly with each individual platform, developers integrate once with the unified API, which handles all the complexity of connecting to underlying services behind the scenes.

Think of it as a universal translator for software systems. Your application speaks one language - the unified API's standardized format - and the unified API instantly converts your requests into the correct format for each connected service, whether that's Salesforce or HubSpot for CRMs, QuickBooks or Xero for accounting, or ADP or Gusto for payroll.

The Core Components

A comprehensive unified API provides three fundamental capabilities:

1. Unified Authentication Instead of implementing OAuth flows, API keys, and authentication protocols for each provider, developers authenticate once through the unified API. Whether your customer uses service A or service Z, the authentication process remains consistent.

2. Normalized Data Models A unified API standardizes data structures across providers. A "contact" object from HubSpot looks identical to a "contact" from Salesforce, even though the underlying APIs structure this data differently. This normalization extends to field names, data types, and object relationships.

3. Synchronized Data Operations The unified API handles bidirectional data sync, ensuring that when you create, read, update, or delete data through the unified interface, those operations are correctly translated and executed across all connected systems.

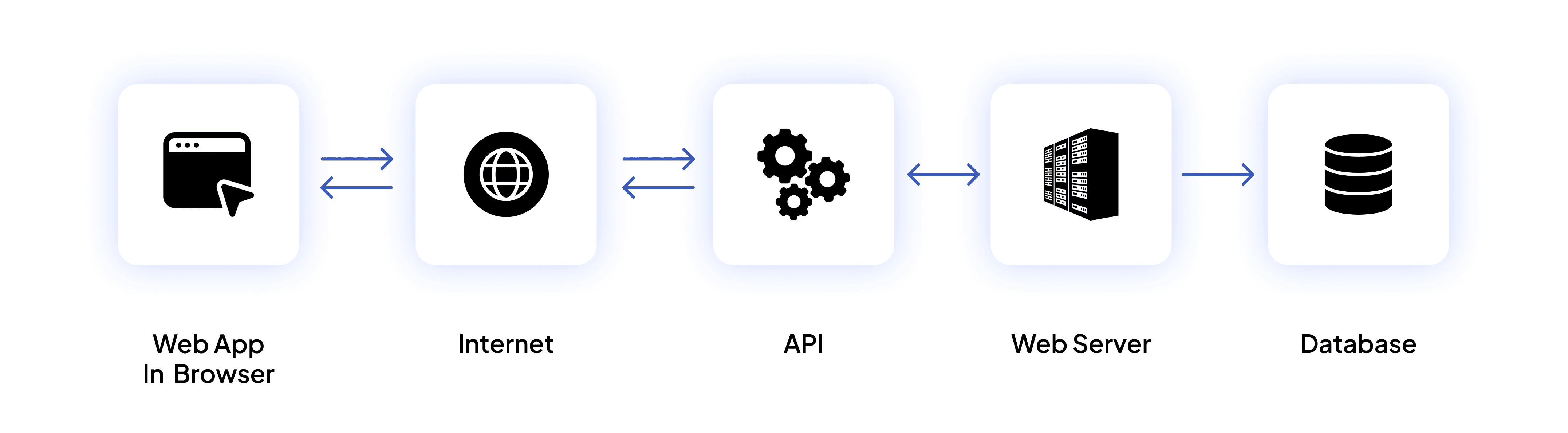

How Unified APIs Work: Under the Hood

When your application makes a request to a unified API, here's what happens:

Request Receipt: Your application sends a standardized API call to the unified API endpoint

Routing: The unified API identifies which underlying service(s) need to be accessed based on the customer's connected accounts

Translation: The request is translated from the unified format into the specific format required by the target system

Execution: The translated request is sent to the provider's native API

Response Normalization: Data returned from the provider is transformed back into the unified API's standardized format

Delivery: The normalized response is sent back to your application

This abstraction layer eliminates the need for your team to understand the idiosyncrasies of each provider while still enabling access to their data and functionality.

The Financial Services Context: Why Unified APIs Matter

The financial services sector presents unique conditions that make unified APIs particularly valuable:

Fragmented Technology Landscapes

Banking and insurance organizations operate in environments where customers use diverse systems. A corporate client might have accounts with five different banks, use three payroll providers across different subsidiaries, and maintain insurance policies from multiple carriers. Financial platforms serving these clients must integrate with all of these systems to provide comprehensive service.

Regulatory Compliance Requirements

Open banking regulations, data protection frameworks, and financial compliance standards add layers of complexity to integrations. Unified API providers often build compliance requirements directly into their abstraction layer, reducing the burden on individual developers to ensure each integration meets regulatory standards.

Real-Time Data Imperatives

Financial decisions often depend on current information. Loan approvals need real-time income verification. Insurance underwriting requires up-to-date risk assessments. Trading platforms need instant account balance checks. The speed advantage of building one integration instead of dozens becomes a competitive differentiator.

Scale Requirements

Financial institutions and fintech platforms don't serve just a few customers - they serve thousands or millions. When each customer potentially uses different underlying systems, the number of integration permutations explodes. Unified APIs make this scale manageable.

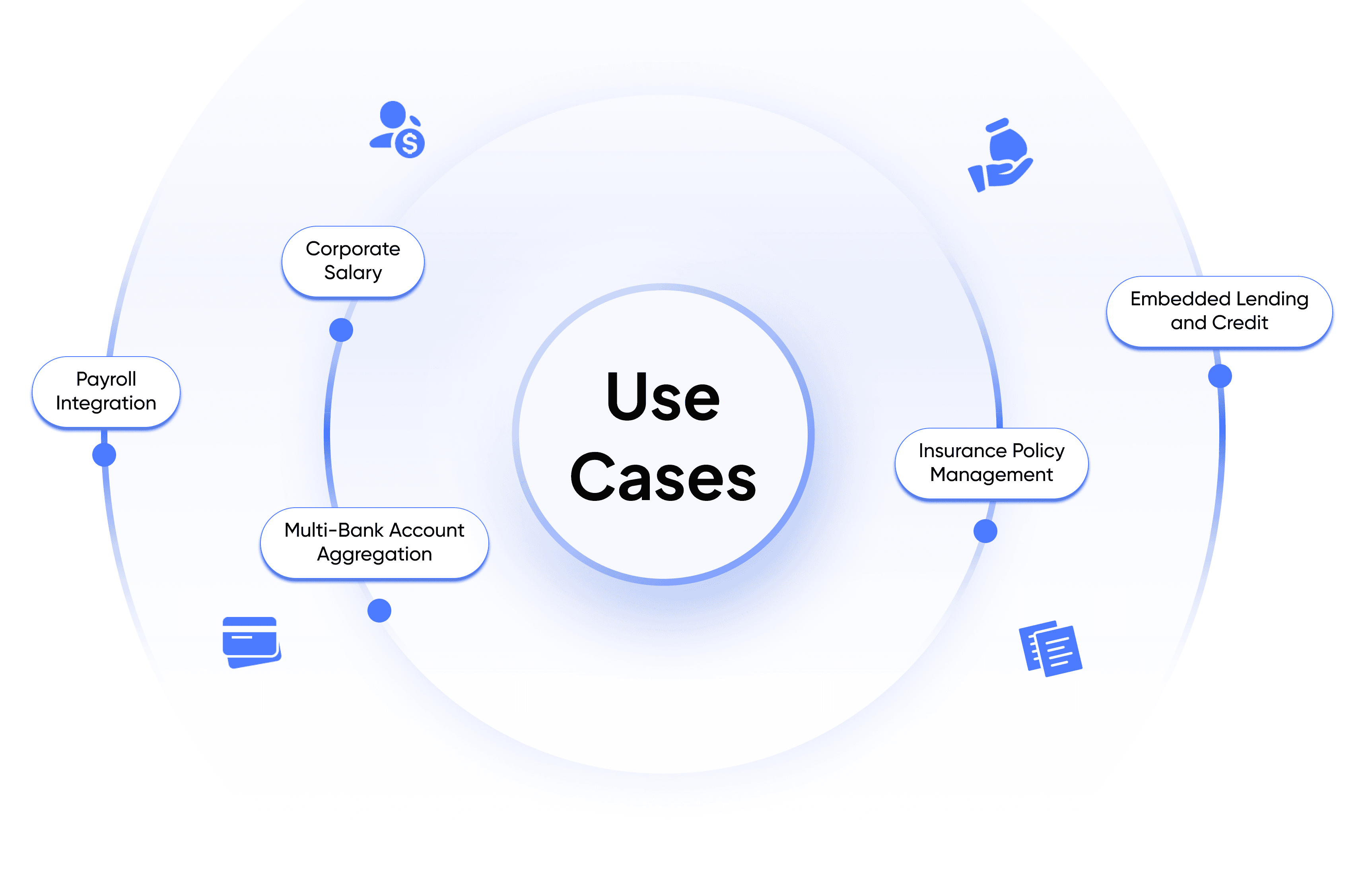

Use Cases Transforming Banking and Fintech

Corporate Salary and Payroll Integration

Consider a benefits administration platform that needs to deduct insurance premiums directly from employee paychecks. Without a unified API, this would require integrating separately with ADP, Gusto, Paychex, Workday, Rippling, BambooHR, and dozens of other payroll systems - each with different API structures, authentication methods, and data formats.

With a unified payroll API (such as those provided by Finch), the benefits platform integrates once and gains access to payroll data across all providers. When an employee enrolls in insurance, the premium deduction is automatically synced to their payroll system, regardless of which one their employer uses. This enables:

Automated premium collection without manual payroll file uploads

Real-time verification of employment and income for loan applications

Instant benefit enrollment for new hires across any HRIS system

Synchronized employee data for 401(k) and retirement account management

Multi-Bank Account Aggregation

Personal finance platforms and wealth management apps need to display financial information from multiple banks in one unified view. Open banking APIs enable this, but connecting to 50+ different banks - each with their own API implementations of open banking standards - represents a massive integration challenge.

Unified banking APIs aggregate these connections, allowing fintech apps to:

Display real-time account balances across all of a user's banks through a single integration

Initiate payments from any connected bank account with standardized commands

Verify account ownership instantly for lending decisions without micro-deposit delays

Categorize and analyze transactions across multiple financial institutions

Insurance Policy Management

Insurance brokers and comparison platforms need to access policy information, submit applications, and process claims across multiple insurance carriers. Each carrier has different systems, data formats, and integration requirements.

A unified insurance API enables:

Multi-carrier quote aggregation in real-time

Automated policy issuance across different insurance providers

Unified claims submission and tracking

Group insurance enrollment for corporate clients using any carrier

Embedded Lending and Credit

Buy-now-pay-later services, digital lending platforms, and embedded finance solutions need to connect with multiple credit providers, banking partners, and risk assessment services. Unified APIs make it possible to:

Offer customers financing options from multiple lenders through one integration

Access real-time credit scoring from multiple bureaus with standardized requests

Enable instant bank account verification for underwriting decisions

Process loan disbursements and repayments across different banking systems

Real-World Impact: The Business Case

The advantages of unified APIs extend beyond technical elegance to deliver tangible business outcomes:

Accelerated Time-to-Market

Organizations using unified APIs report reducing integration development time from 12-18 months to 6-8 weeks. This acceleration means features reach customers faster, competitive advantages are realized sooner, and revenue generation begins earlier.

Resource Efficiency

Instead of dedicating engineering teams to building and maintaining dozens of point-to-point integrations, organizations can reallocate those resources to core product development. The cost savings are significant - one integration to maintain instead of fifty.

Improved Customer Experience

When integration complexity is managed through a unified API, end users benefit from smoother onboarding (they can connect whatever systems they already use) and more reliable service (with unified error handling and monitoring).

Scalability Without Complexity

As organizations grow and need to support additional platforms, unified APIs make expansion straightforward. Adding support for a new payroll system or bank simply means waiting for the unified API provider to add that connector - not tasking your engineering team with a multi-month integration project.

Considerations and Trade-offs

While unified APIs offer compelling advantages, they're not without limitations:

Depth vs. Breadth

Unified APIs must balance supporting many platforms with supporting advanced features of each platform. The more providers a unified API supports, the more it must adhere to a "lowest common denominator" data model. Provider-specific features that don't exist across all platforms may not be accessible through the unified interface.

Dependency on the Provider

Using a unified API means your integration infrastructure depends on a third-party vendor. Their roadmap determines which new platforms you can support, their uptime affects your service reliability, and their pricing model impacts your costs.

Real-Time vs. Cached Data

Some unified API providers cache data to improve performance and manage rate limits from underlying services. Others fetch data in real-time with each request. The choice affects data freshness and needs to align with your use case requirements. Financial applications often need real-time data, making this an important evaluation criterion.

Customization Constraints

Enterprise clients often require highly specific, bespoke integrations that leverage unique features of their chosen platforms. Unified APIs' standardized approach may not accommodate these custom requirements, necessitating supplementary point-to-point integrations for specific clients.

Evaluating Unified API Providers

For organizations in banking, fintech, and insurance considering unified APIs, key evaluation criteria include:

Coverage: Does the provider support the platforms your customers actually use? For Indian markets, this might mean local payroll providers, Indian banks implementing UPI, and regional insurance carriers.

Data Model Completeness: Does the unified data model include all the fields and relationships you need for your use cases?

Authentication Flexibility: How does the provider handle complex authentication scenarios, particularly in highly regulated financial environments?

Real-Time Capabilities: Does the provider offer actual real-time data access or rely on periodic synchronization?

Compliance Features: Are regulatory requirements (data residency, audit logging, consent management) built into the platform?

Transparency: Can you access raw responses from underlying APIs when needed, or does the abstraction layer block visibility entirely?

Webhooks and Events: How does the provider handle real-time notifications when data changes in underlying systems?

The Future: From APIs to API Ecosystems

The unified API model is evolving. Forward-looking providers are expanding beyond single categories (like "payroll" or "banking") to create comprehensive financial data ecosystems. Emerging trends include:

Multi-Category Platforms: Unified APIs that span HRIS, payroll, benefits, banking, accounting, and insurance in one platform

AI-Enhanced Data Mapping: Machine learning to automatically map custom fields and objects across providers

Embedded Compliance: Built-in regulatory compliance for multiple jurisdictions, automatically updated as regulations change

Composable Finance: Unified APIs serving as building blocks for embedded finance experiences

Conclusion

Unified APIs represent a fundamental shift in how financial services organizations approach integration challenges. By abstracting away the complexity of connecting to multiple systems and providing a single, standardized interface, they enable banks, fintechs, and insurance companies to focus on building differentiated products rather than wrestling with integration complexity.

For a fintech platform enabling salary-linked insurance, a bank building multi-institution account aggregation, or an insurance broker offering multi-carrier quotes, unified APIs transform what was once a multi-year engineering initiative into a weeks-long implementation.

As financial services continue their digital transformation, the organizations that can most quickly and reliably integrate with the diverse systems their customers use will have a decisive competitive advantage. Unified APIs provide the technical foundation to achieve that speed and reliability at scale.

The question for financial services leaders is no longer whether to leverage unified APIs, but which use cases to prioritize first and which unified API providers align best with their strategic objectives. In an industry where data flows are the lifeblood of service delivery, mastering the integration layer through unified APIs may well determine who leads the next decade of financial innovation.

Tartan helps teams integrate, enrich, and validate critical customer data across workflows, not as a one-off step but as an infrastructure layer.