How Fintech Industry Can Improve Credit Underwriting By Looking Beyond Credit Score?

What is Credit?

When lenders offer credit to borrowers, they want to ensure that the borrowers have creditworthiness. Often credit score is the only factor used in evaluating customers.

In India, the four major credit reporting agencies are – CRIF High Mark, Experian, TransUnion CIBIL, and Equifax. Credit scores vary anywhere from 300 to 900. The higher the score, the better will be the offers from lenders. If the borrower has a credit score higher than 750, lenders will consider them as a low-risk borrower and may offer much better interest rates.

How Traditional Credit Underwriting Is Done

Credit underwriting was a hugely manual process until a few years ago. Lenders went through loan papers manually to determine the creditworthiness of borrowers. Credit scores were considered a key metric to determine the likelihood of repayment by the borrower also known as the ability to repay. This excluded millions of customers because credit bureau reports were erroneous and incomplete. FinTech companies use algorithms and mathematical calculations to determine repayment capability and consider data beyond the credit score to determine creditworthiness.

Why Look At Alternative Sources of Data

According to Researchscape, an independent research firm, about 74% of lenders believe that traditional credit reports and credit scores are inaccurate in determining creditworthiness. In the same report, it was clear that 59% of lenders are looking at alternative data for credit underwriting.

Consumer affordability calculations now include multiple data points such as cash flow, rent payment, and utilities. These additional data provide more information on short-term and long-term risk factors for a customer. FinTech companies are looking to expand their banking services and tap into the untouched market. So, 90% of lenders need alternative data points such as payroll system data that will help them gain access to new consumer segments.

Alternative financial data is not only used in credit underwriting, but they are also useful in fraud detection, account management, pricing, marketing, and servicing. The speed and accuracy of creditworthiness evaluation greatly increase using alternative data. It is also useful for customers because, with enhanced assessments, they can access additional banking products and favorable pricing terms. It also improves automated underwriting, eliminating human bias.

Cash flow evaluation provides a more comprehensive report on customers’ reliable income patterns from multiple sources beyond a single job. Consumers grant their permission expressly, and this allows more scope for transparency. Utility payment history data provides insight into the payment regularity of the customer. This evaluation with alternative data greatly improves inclusion, especially for those who cannot get a loan otherwise. It increases opportunities for lenders to offer financial products customized for each consumer.

Importance of Alternative Data & How Tartan Enables FinTech Companies

More than 65% of lenders believe that the banking systems and FinTech industry will adapt to alternative data within the next five years. After all, with digitisation happening everywhere, the industry is ready for an overhaul incorporating new techniques for credit underwriting.

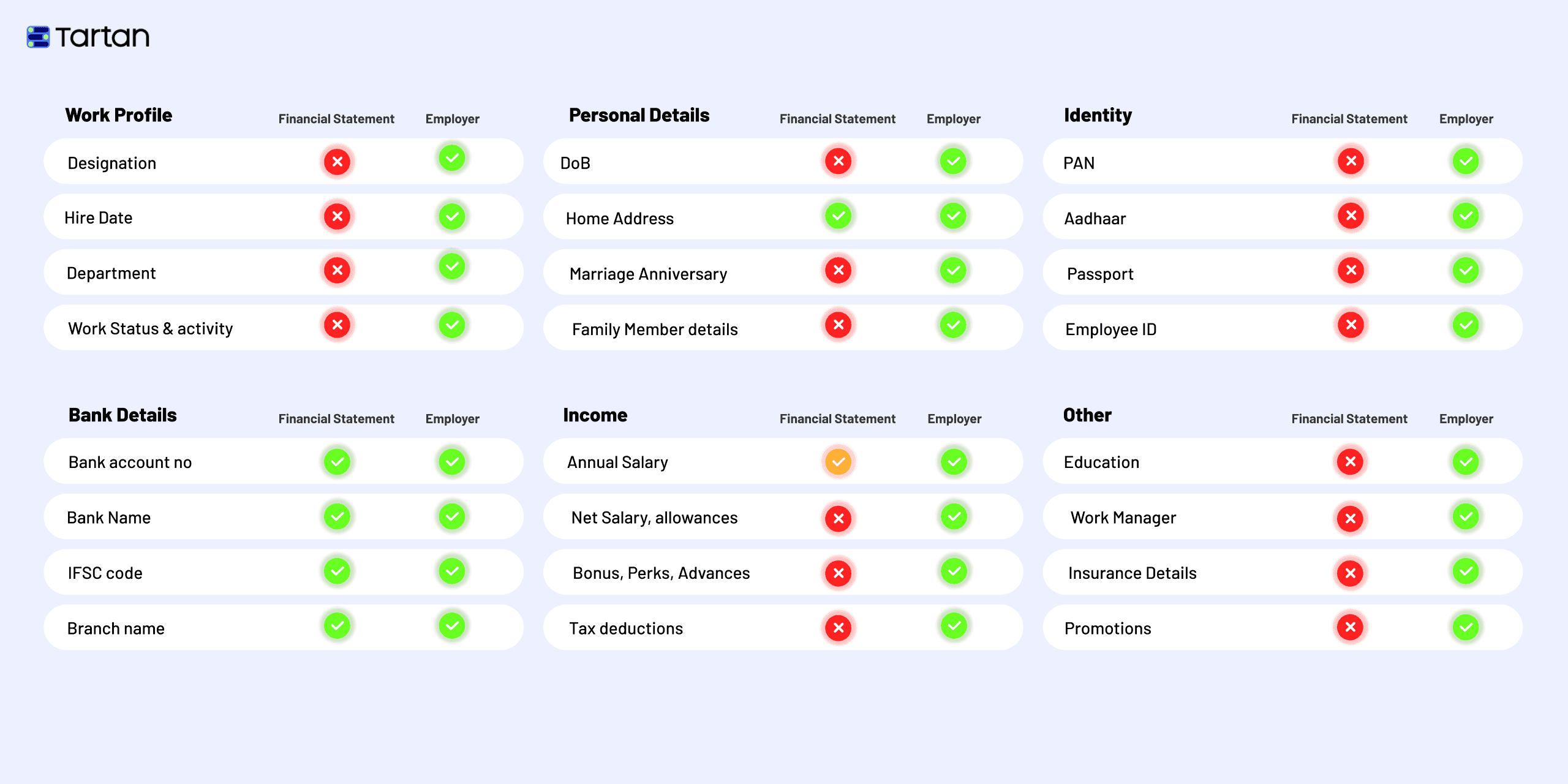

1. Alternative data, including non-transaction checking accounts, employment data, income verification data, cash flow, bank transaction data, rent payment, utility payment, and deep subprime data, provide a clearer picture of an individual's credit situation.

2. Alternative data is useful in predicting underwriting processes.

3. Additional data points are useful in reaching new audiences.

4. 23% of lenders want to adopt new data sources as a part of their credit risk assessment.

Upgrading tested credit risk assessment is a huge step for FinTech companies, and there are many barriers. Lenders worry about the reliability of alternative data and the cost involved in data analytics. Many companies worry that loss avoidance projections may not match up to realistic data. Technology is also a major barrier.

This is where a company like Tartan can help FinTech companies quickly adapt new technologies to include alternative data for credit underwriting. By verifying customer details quickly, effectively, and accurately, lenders can rest assured knowing that the risk associated with each borrower is carefully understood. By outsourcing verifications to a technologically sound company, lenders can quickly use the final reports and data to process loan applications.

Conclusion

The credit risk assessment is going through a digital transformation as 50% of lenders are ready to adopt alternative data, while 39% are already using it. Access to alternative data analytics will help lenders revamp their credit underwriting process and improve customer experience. It will also help reach a huge market share by gaining access to an untapped audience.

Tartan is a payroll connectivity and full-stack verification bank API company enabling consent-driven employment and income verification in real time. We help simplify banking by eliminating reliance on manual processes for income and employment verifications and KYC-related verifications. Tartan quickly assesses creditworthiness in real-time to make accurate risk assessments with over 30+ accurate and verified data points.

Click here, to know more about how Tartan can help you with alternative data.