Every NBFC with a salaried lending product has the same conversation internally at some point. The LOS is modern. The credit model is reasonably well-tuned. The bureau integrations are live. And yet the loan TAT - from application to disbursal - is still measured in days rather than hours, and the ops team is still chasing the same bottleneck it has always chased.

Employment verification.

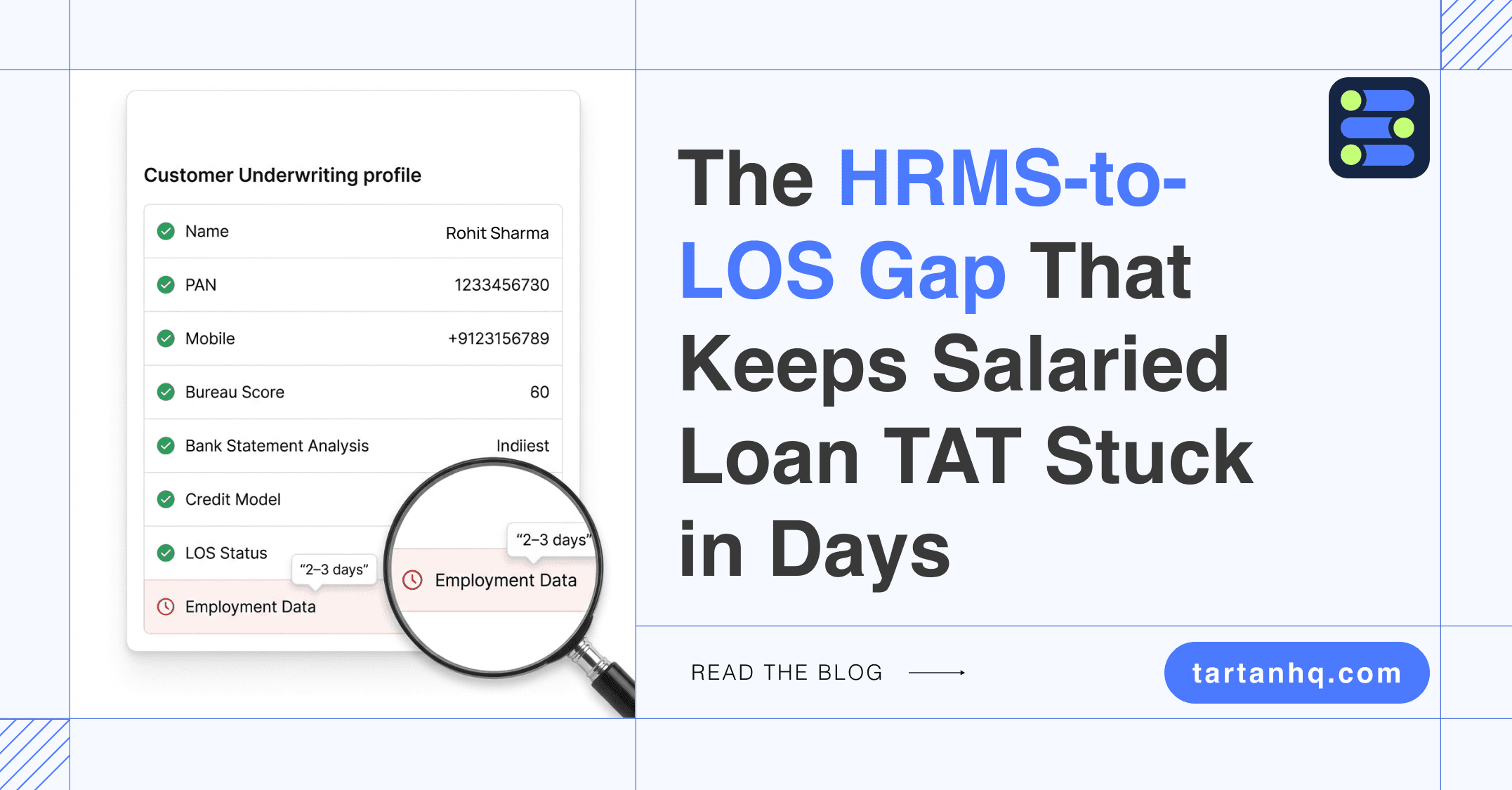

The applicant works at a company. The company runs an HRMS. That HRMS contains, right now, exactly what the LOS needs to make a credit decision - current employment status, monthly gross salary, date of joining, designation, department. The data is verified, current, and sitting in a system the employer updates as a matter of daily routine.

Getting it into the LOS, however, requires a human to carry it across. The applicant downloads a salary slip, uploads it to the portal. Someone on the ops team looks at it, possibly runs it through an OCR tool, manually keys the relevant fields into the credit system.

If the slip is unclear, they ask for another one. If the employment details need confirmation, they ask for a letter. The whole sequence takes anywhere from a few hours to a few days depending on applicant responsiveness and ops bandwidth.

This is the HRMS-to-LOS gap. It is the single most unnecessary bottleneck in the salaried lending workflow - unnecessary because the data exists, is accurate, and is accessible. The problem is not data availability. It is data connectivity.

Why this specific gap persists

NBFCs have invested heavily in LOS modernisation. Bureau integrations, bank statement analysers, GST-based underwriting for MSMEs, AI-assisted decisioning - the infrastructure around the credit decision has been upgraded substantially in the last three years.

TAT improvements have followed.

But employment verification has largely been left behind. The reason is partly structural and partly a legacy of how salaried lending was built - around documents as the unit of verification rather than live data sources.

Salary slips, Form 16, employment letters - these were the inputs the credit model was trained on, and the ops process was built around collecting them. Digitising document collection made the process faster. It did not change its architecture.

The result is that in 2025, an NBFC’s LOS can pull bureau data in seconds, analyse six months of bank statements in minutes, and run a credit decision model in real time - and then sit idle for 24 hours waiting for a salary slip the applicant hasn’t uploaded yet.

“The modern NBFC’s LOS is fast everywhere except where employment verification sits. That one step - still dependent on a document a human provides - is the gap that undoes the rest of the investment in TAT.”

What the gap actually costs

Let’s be specific, because the cost of this gap is larger than most NBFCs have formally calculated.

Drop-off. Every hour between application and decision is an hour during which the applicant may go to a competitor, lose interest, or simply forget to complete the process.

In salaried lending, where the borrower typically has multiple options, TAT is a conversion variable. NBFCs that have reduced verification TAT from 48 hours to under four report measurable improvements in application-to-disbursal conversion.

The employment verification step - waiting for the applicant to submit a document - is a primary driver of the hours lost in that window.

Ops cost. Manual verification is expensive in proportion to volume. A team processing a few hundred applications a day spends a significant portion of its time on employment verification tasks - checking salary slip authenticity, confirming employment details, following up with applicants who submitted incomplete documents.

This is not value-adding work. It is document logistics. At scale, it represents a meaningful headcount cost that compounds as loan volumes grow.

Data quality and fraud exposure. Salary slips can be fabricated. They are among the most commonly forged documents in retail lending fraud in India. OCR tools catch some forgeries; they miss others.

The fundamental problem is that a document the applicant provides is a document the applicant controls - and any verification process built on applicant-provided documents has an inherent integrity gap. Employment data pulled directly from an employer’s HRMS, with the employer’s consent, has no equivalent gap. The employer has no incentive to misrepresent it, and the applicant has no ability to alter it.

Credit model accuracy. A credit model trained on salary slip data is a model trained on a snapshot that may be weeks old at the time of application. An applicant who received a notice period letter the day after their last salary slip was issued looks identical to an employed applicant in every signal the document provides. Live HRMS data surfaces this. A document does not.

48hrs typical salaried loan TAT waiting on employment verification | Real-time what HRMS-to-LOS direct connect makes possible | 80+ HRMS platforms coverable via a single unified API |

What direct HRMS-to-LOS connectivity looks like

When an NBFC connects its LOS to a live HRMS data source - rather than waiting for the applicant to provide documents - the verification workflow changes structurally.

The applicant submits their loan application. As part of the flow, they are prompted to authorise a consent-based connection to their employer’s HRMS - a single authentication step that takes under a minute.

The LOS pulls employment data directly: current employment status confirmed, monthly gross salary retrieved, date of joining calculated into tenure, designation and department verified.

This happens in seconds. Not hours. The LOS has everything it needs to complete the employment verification component of the credit assessment before the applicant has finished reading the confirmation screen.

The credit officer’s queue no longer has a “pending employment documents” status. The applications that would previously have sat for 24 hours waiting for a salary slip are now fully verified and ready for decision. The ops team’s verification workload for salaried applications drops sharply. The drop-off window between application and disbursal compresses.

Beyond speed, the quality of the data changes. The NBFC is now underwriting on verified, current employment data - not a document the applicant chose to provide. Employment status as of today. Salary as of the current payroll cycle.

Tenure calculated precisely from the HRMS joining date. If anything material has changed since the applicant’s last salary slip - a resignation submitted yesterday, a role change last week - the HRMS reflects it. The document would not.

The portfolio quality argument

There is a credit risk dimension to this that deserves more attention than it typically receives in TAT-reduction discussions.

Research on Indian lending consistently finds that loans processed faster - when supported by structured, verified data - tend to perform better than loans that moved slowly through manual verification.

The intuition is straightforward: a fast decision backed by live data is more accurate than a slow decision backed by old documents. The borrower whose current employment status is confirmed at the moment of application is a better-underwritten credit than one whose status was confirmed via a document issued three weeks earlier.

For an NBFC managing a large salaried portfolio, improving the quality of employment verification at origination is not just an operations efficiency play. It is a portfolio quality play. The defaults that trace back to stale employment data at the time of underwriting - borrowers who were in notice period, had salary revisions that weren’t reflected in their slips, or had left the company entirely - are the defaults that live employment verification eliminates before they happen.

The HRMS diversity challenge - and how to solve it once

The practical challenge NBFCs face when trying to build this is that their applicants come from companies running dozens of different HRMS platforms.

A salaried portfolio of any scale will include employees from companies using Darwinbox, GreytHR, Keka, SAP SuccessFactors, Zoho People, and a long tail of others. Building a direct integration with each of these is not a lending project - it is a multi-year infrastructure project that falls well outside the competency and resource envelope of most NBFC tech teams.

This is the specific problem a unified employment data API solves. One integration. One data model. Coverage across 80+ HRMS platforms.

When an applicant authorises the connection, the system identifies their employer’s HRMS, authenticates, and returns standardised employment data - regardless of which platform their employer uses.

The NBFC’s LOS does not need to know or care which HRMS is on the other side.

It receives the same clean, structured data every time.

Where HyperSync fits into the LOS workflow

Tartan’s HyperSync is built precisely for this integration point. It sits between the LOS and the employer’s HRMS - a consent-driven, real-time employment data layer that covers 80+ HRMS platforms under a single API.

NBFCs integrating HyperSync into their loan origination workflow get live employment verification at the point of application, with data that is current, verified, and sourced directly from the employer’s system of record.

The integration is lightweight on the NBFC’s side - a single API connection that fits into the existing LOS data flow. Go-live is measured in days, not sprints. And the data model is standardised across all HRMS platforms, so the credit team and the model get consistent, structured inputs regardless of where the applicant works.

TAT reduction in salaried lending has a ceiling as long as employment verification depends on documents. NBFCs that have modernised everything else in their origination stack but left this step untouched are leaving the single largest remaining improvement on the table.

The data your LOS needs is already sitting in your applicant’s employer’s HR system. The only question is whether there is a live connection between the two - or whether a human is still carrying it across by hand.